The Residential Care Subsidy (“Subsidy”) is becoming increasingly topical as New Zealand’s 65+ population is projected to increase from 15% in 2016 to over 25% by 2068. The growth in this population will increase the number of Subsidy applications for financial assistance for long-term residential care in a rest home or hospital (“Care”). Despite the predicted growth in applications, many New Zealanders are not aware that their current asset planning has the potential to affect the outcome of a Subsidy application significantly. In light of this, advice surrounding asset planning in consideration of a Subsidy application is essential.

The Ministry of Social Development (“MSD”) determines Subsidy applications. When considering an application, they will conduct a financial means assessment to determine whether the applicant qualifies under the prescribed eligibility thresholds. This includes both an asset and an income assessment.

Before the applicant undertakes the income assessment, MSD will first assess whether they qualify under the asset assessment (“Assessment”). The asset thresholds for the Subsidy are as follows:

- A single applicant or applicants that have a partner in Care: The total value of their assets must not exceed $224,654.00 including the value of the family home and vehicle;

- Applicants who have a partner that is not in Care can elect to be assessed under either of the following thresholds:

- Their assets must not exceed $123,025.00 (not including the value of the family home and vehicle); or

- The total value of all their assets (family home and vehicle included) must not exceed $224,654.00.

The Gifting Provisions

MSD implemented gifting thresholds to prevent the giving away of assets with the purpose of attempting to qualify under the asset thresholds for the Subsidy.

Gifting thresholds apply to gifting commonly, i.e. birthday gifts, and gifting undertaken to a Family Trust (“Trust”). Gifting to a Trust is when an individual (“Settlor(s)”) who owns assets such as houses, cash and shares, sells these assets into a Trust. In return, the Trust owes a debt back to the Settlor(s). The debts are then “forgiven” by the Settlor(s) through a process called gifting.

The MSD gifting thresholds are:

- Five years before applying for the Subsidy each person can gift up to $6,000.00 each annually. In this case, those in a qualifying relationship under the Property (Relationship) Act 1976 (“relationship”) may gift $6,000.00 each.

- Beyond five years before the Subsidy application, a couple or individual can gift up to $27,000.00 annually. In this case, those in a relationship may gift up to $12,500.00 each.

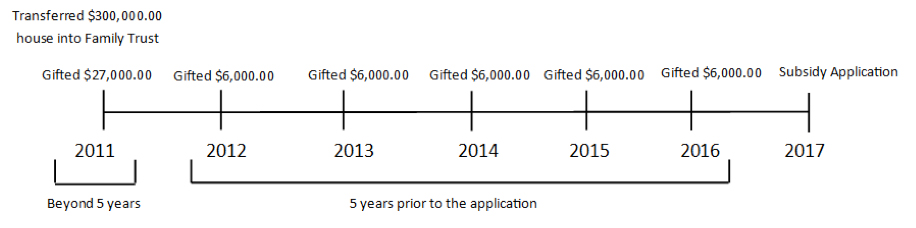

Gifting that falls under the prescribed gifting thresholds will not be considered in the Assessment. However, if an applicant has sold an asset into a Trust that exceeds the gifting threshold, MSD will consider the value of the asset that exceeds the gifting thresholds as a personal asset. For example, an applicant sells their house valued at $300,000.00 to their Trust in 2011 and gifts annually until 2016; they apply for the Subsidy in 2017. MSD will subtract the value of the prescribed gifting being $27,000.00 in 2011 and $6,000 annually until 2016. The remaining $243,000.00 will be considered a personal asset under the Assessment. The applicant would not qualify for the Subsidy in this instance.

Please see diagram below which offers a visual aid to the implementation of the MSD gifting thresholds:

If the same applicant had a partner who was not in Care, it may have been more beneficial for the applicant to hold the property as a personal asset. If the house was a personal asset, in this case, they could be considered under the eligibility threshold which excludes the value of the family home and vehicle if they chose. The applicant would qualify for the Subsidy in this instance.

Please note MSD will only consider gifting to a Trust that has been completed and will not take into account any entitled gifting that has not been completed.

Recommendations:

- Plan in advance. If a Subsidy application is likely, and you own a trust; implement a consistent gifting regime so that you can take advantage of MSD’s prescribed gifting thresholds.

- If you already have a trust or are considering forming a trust and may apply for the Subsidy, consider seeking legal advice on your position, including whether you could consider selling your home out of your Trust to meet the Assessment.

Please note that this article only covers aspects of a Subsidy application. For more comprehensive advice, please seek legal counsel.